Key Takeaways

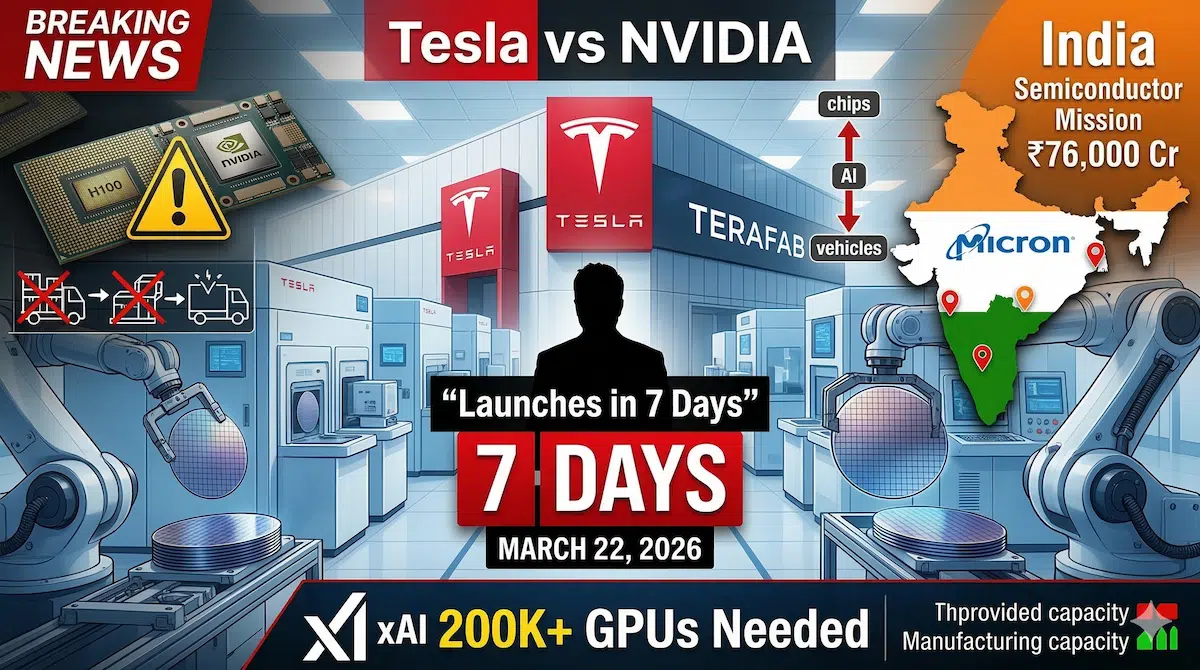

- Elon Musk announced Tesla Terafab semiconductor manufacturing facility launches March 22, 2026—seven days from his March 15 declaration — The $10+ billion vertical integration play positions Tesla to produce custom AI chips in-house for vehicle autopilot systems and xAI’s massive language model training, directly challenging NVIDIA’s GPU monopoly as semiconductor shortages continue strangling AI infrastructure buildouts globally

- India’s ₹76,000 crore semiconductor mission faces critical test as global chip race intensifies with Tesla and Micron expansion announcements — Micron Technology revealed second fab construction on same day as Musk’s Terafab declaration, validating persistent chip shortage that’s delayed India’s $200 billion AI infrastructure commitments including Adani’s data centers and IndiaAI Mission’s GPU procurement targeting 1.8 million units by 2027

- Tesla’s vertical integration from chips to AI models mirrors Apple’s strategy but targets AI compute infrastructure market worth $600 billion in 2026 alone — xAI requires 200,000+ H100-equivalent GPUs for Grok-3 training but NVIDIA allocation constraints forced Musk’s decision to manufacture Tesla’s own chips, creating competitive threat to NVIDIA’s 80%+ AI chip market share and potentially opening India partnership opportunities if domestic production capacity proves attractive versus US-China tensions

On March 15, 2026, Elon Musk posted a characteristically cryptic update that sent semiconductor industry analysts scrambling: “Terafab launches in 7 days.” By March 16, leaked internal Tesla documents and supplier confirmations revealed Terafab represents Tesla’s ambitious entry into semiconductor manufacturing—a $10+ billion facility designed to produce custom AI chips for Tesla vehicles and xAI’s computational infrastructure, launching March 22, 2026.

The timing intersects directly with India’s semiconductor ambitions and ongoing chip shortage crippling the country’s AI infrastructure expansion. As Musk announces vertical integration into chip manufacturing, India’s ₹76,000 crore semiconductor mission struggles to attract major fabrication plants beyond Micron’s memory chip commitment. The question facing Indian policymakers: Can India position itself as an alternative manufacturing location for Tesla’s chip production ambitions, or will the country remain dependent on imported semiconductors while spending $200+ billion building AI data centers that lack sufficient compute hardware?

The semiconductor shortage isn’t theoretical for India. Adani’s $100 billion renewable AI data center pledge announced at the India AI Impact Summit requires tens of thousands of GPUs and AI accelerators that simply aren’t available at scale. IndiaAI Mission’s existing 18,693 GPUs represent a starting point, but scaling to 1.8 million units—the quantity implied by Elon Musk’s “10x compute equals 2x intelligence” scaling law for achieving GPT-5 level capabilities—requires either massive imports subject to geopolitical constraints or domestic production capacity India doesn’t currently possess.

Why Tesla Needs Its Own Chips: The xAI Bottleneck

Tesla’s chip manufacturing ambitions aren’t primarily about vehicles, despite autopilot systems consuming significant compute. The real driver is xAI, Musk’s AI company training Grok language models to compete with OpenAI’s GPT series and Google’s Gemini. xAI’s Grok-3 model, currently in training, requires computational infrastructure comparable to Meta’s Llama 3 or Google’s Gemini 2—meaning 200,000 to 400,000 H100-equivalent GPUs running continuously for months.

NVIDIA can’t supply that volume to any single customer in 2026. The company allocates H100 and newer H200 chips across hundreds of customers—hyperscalers like Amazon, Google, and Microsoft receive priority, with startups and individual companies getting whatever remains. Musk publicly complained in January 2026 that xAI’s GPU allocation from NVIDIA was “embarrassingly inadequate” given xAI’s $6 billion Series B funding and ambitious model development timeline.

Terafab solves this problem through vertical integration. If Tesla manufactures its own AI training chips—even if initially less powerful than NVIDIA’s latest generation—the company controls supply completely. A chip that’s 70% as efficient as NVIDIA’s H200 but available in unlimited quantities beats waiting 18 months for H200 allocation. Tesla’s automotive manufacturing expertise in scaling production, supply chain management, and quality control translates directly to semiconductor fabrication once the technical knowledge and fabrication equipment are acquired.

The financial logic mirrors Apple’s M-series chip strategy. Apple spent billions developing custom silicon to replace Intel CPUs, accepting initial performance compromises for long-term control over its hardware-software integration and supply chain independence. Apple now designs industry-leading chips that outperform competitors while capturing margin that previously went to Intel. Tesla aims for identical economics in AI chips—capture the margin NVIDIA currently extracts while ensuring xAI never faces compute constraints.

India’s Semiconductor Mission: Can It Attract Tesla?

India’s ₹76,000 crore ($9.1 billion) semiconductor mission, announced in December 2021 and expanded through 2024-2025, aims to establish India as a global chip manufacturing hub. The program offers financial incentives covering up to 50% of project costs for companies building fabrication plants, assembly facilities, and design centers in India.

Results remain modest. Micron Technology committed to a $2.75 billion assembly and test facility in Gujarat, operational by late 2024. Tata Electronics partnered with Taiwan’s Powerchip Semiconductor Manufacturing Corporation for a fab in Gujarat targeting 2026 production start. CG Power announced plans for a compound semiconductor fab. But India hasn’t attracted a leading-edge logic chip manufacturer—the type producing CPUs, GPUs, and AI accelerators that actually power data centers and AI training.

Tesla’s Terafab represents exactly the category India needs but hasn’t secured. If Musk genuinely intends large-scale AI chip production, India offers compelling advantages versus US-only manufacturing:

Labor cost arbitrage: Semiconductor fabrication requires thousands of engineers and technicians. Indian engineering talent costs 60-70% less than equivalent US workers, directly impacting operational expenses for a fab running 24/7 operations.

Government incentives: India’s 50% capital subsidy could reduce Tesla’s fab construction costs from $10 billion to $5 billion, with additional tax breaks and infrastructure support. US CHIPS Act offers subsidies but with more regulatory requirements and political constraints.

Geopolitical diversification: US-China tensions create supply chain risks for any company manufacturing exclusively in either country. India represents a neutral third option, particularly valuable if Tesla wants to sell vehicles and AI services in both markets without dependency on either.

Market access: India represents Tesla’s largest untapped automotive market and a massive AI services opportunity. Local chip production supports “Make in India” requirements for government contracts and reduces import duties on finished vehicles containing Indian-made components.

The obstacles are equally significant. India lacks advanced semiconductor ecosystem—equipment suppliers, specialty chemical manufacturers, ultra-pure water facilities, and the tacit knowledge embedded in Taiwan’s TSMC or South Korea’s Samsung manufacturing processes. Building a leading-edge fab in India requires importing nearly everything initially, from lithography equipment (ASML monopoly based in Netherlands) to engineering expertise (likely poached from TSMC or Samsung). Power grid reliability concerns persist despite renewable energy commitments. Regulatory complexity and approval timelines in India often exceed those in the US or Taiwan.

The Broader Chip Shortage and India’s AI Infrastructure Risk

Micron Technology’s announcement on March 15, 2026—the same day as Musk’s Terafab declaration—that it’s building a second memory chip fab underscores the persistent semiconductor shortage. Micron specifically cited AI data center demand for high-bandwidth memory (HBM) used in GPU systems. Every NVIDIA H100 or H200 GPU requires specialized memory chips that only Micron, Samsung, and SK Hynix manufacture, and production can’t scale fast enough to meet demand.

This shortage directly threatens India’s AI ambitions. The $200+ billion committed to AI infrastructure at the India AI Impact Summit—Adani’s $100 billion, Microsoft’s $50 billion expansion, Blackstone’s $600 million, government’s $1.1 billion—assumes ability to purchase and deploy AI hardware at scale. But if Tesla, Meta, Google, Amazon, and Microsoft are competing for the same constrained GPU supply, and now companies like Tesla are vertically integrating to bypass the market entirely, India’s infrastructure projects face either extended delays or massive cost increases.

IndiaAI Mission allocated ₹10,372 crore ($1.25 billion) total across seven pillars, with perhaps ₹3,000-4,000 crore for compute infrastructure. That funded the existing 18,693 GPUs. Scaling to 1.8 million GPUs at ₹13 lakh per unit (current H100 pricing) requires ₹2.4 lakh crore ($30 billion)—20 times the current budget and 12% of the entire $200 billion infrastructure commitment.

The mismatch between infrastructure investments (data centers, power generation, cooling systems, real estate) and actual compute hardware budgets repeats the problem identified in the Morgan Stanley analysis: India is building parking garages without budgeting for cars. If chip shortages persist through 2026-2027 as Micron’s fab expansion suggests, India’s data centers may sit partially empty while customers lack GPUs to deploy in them.

Vertical Integration: The New Competitive Moat

Tesla’s Terafab strategy represents a broader trend reshaping technology competition in 2026. Apple pioneered vertical integration with M-series chips replacing Intel. Google designs TPUs (Tensor Processing Units) for its own data centers rather than buying NVIDIA exclusively. Amazon developed Graviton CPUs and Trainium AI chips. Meta announced custom silicon for AI inference workloads. Microsoft is designing chips for Azure data centers.

The pattern: hyperscalers and well-funded technology companies are internalizing semiconductor design and increasingly manufacturing, capturing margin while ensuring supply. NVIDIA’s 80%+ market share in AI training chips makes it simultaneously indispensable and a strategic vulnerability. No CEO wants their company’s AI roadmap constrained by another company’s allocation decisions.

For India, this trend creates both opportunity and risk. The opportunity: if vertical integration becomes standard, India could attract multiple companies seeking manufacturing diversification, expanding beyond trying to lure one massive TSMC-scale fab. The risk: if every major AI company builds its own chips, the commodity GPU market India planned to buy from may shrink, with cutting-edge hardware available only to vertically integrated giants India’s startups and enterprises can’t access.

India’s strategic response should emphasize partnerships with vertically integrating companies over trying to build a complete semiconductor ecosystem from scratch. Attracting Tesla’s Terafab, even as a minority partner or assembly location for some production stages, would provide more immediate benefit than waiting years to develop indigenous capabilities. Similarly, convincing Google, Amazon, or Microsoft to manufacture their custom chips partially in India leverages their design expertise while building Indian manufacturing capacity and talent.

The semiconductor race isn’t won by any single country or company—it’s too complex, capital-intensive, and dependent on global supply chains. But India risks being left behind if it continues investing heavily in AI infrastructure (data centers, power generation) while remaining entirely dependent on imported chips from increasingly constrained suppliers. Musk’s Terafab announcement, whether it results in India opportunities or not, should accelerate India’s urgency around securing actual chip production capabilities rather than just assembly and packaging facilities.

FAQs

What is Tesla Terafab and why did Elon Musk announce it now?

Tesla Terafab is Tesla’s semiconductor manufacturing facility designed to produce custom AI chips in-house for Tesla’s autonomous vehicle systems and xAI’s language model training infrastructure. Musk announced on March 15, 2026 that “Terafab launches in 7 days” (March 22, 2026), revealing the project after months of supplier leaks suggested Tesla was acquiring chip fabrication equipment. The timing reflects urgency around xAI’s GPU shortage—xAI’s Grok-3 model requires 200,000+ H100-equivalent GPUs but NVIDIA can’t supply that volume to any single customer in 2026 due to allocation constraints across hundreds of AI companies. By manufacturing its own chips, Tesla ensures xAI never faces compute bottlenecks regardless of NVIDIA’s supply decisions. The vertical integration strategy mirrors Apple’s M-series chip development, accepting initial performance tradeoffs for long-term supply chain control and margin capture.

Can India attract Tesla’s chip manufacturing or is Terafab US-only?

Tesla hasn’t confirmed Terafab’s physical location, but industry analysts assume initial US-based manufacturing given existing Tesla facilities in Texas and Nevada plus CHIPS Act subsidies for domestic semiconductor production. However, India represents a compelling alternative or secondary location for several reasons: India’s ₹76,000 crore semiconductor mission offers up to 50% capital subsidies (potentially reducing Tesla’s $10+ billion fab costs to $5 billion), Indian engineering talent costs 60-70% less than US equivalents for 24/7 fab operations, geopolitical diversification away from US-China tensions benefits global supply chain resilience, and local production supports Tesla’s automotive market entry in India while meeting “Make in India” requirements for government contracts. Major obstacles include India’s lack of advanced semiconductor ecosystem (lithography equipment, specialty chemicals, ultra-pure water facilities), need to import initial expertise from TSMC/Samsung, power grid reliability concerns, and regulatory complexity. India should proactively engage Tesla on partnership opportunities rather than assuming US-only production.

How does Tesla’s chip manufacturing affect India’s ₹76,000 crore semiconductor mission?

Tesla’s Terafab announcement validates the strategic importance of semiconductor manufacturing while exposing India’s limited progress attracting leading-edge fabs. India’s mission launched December 2021 with ₹76,000 crore in incentives but has secured only Micron’s $2.75 billion assembly facility and Tata’s partnership with Powerchip for older-generation chips—no leading-edge logic chip manufacturing for AI accelerators, CPUs, or advanced GPUs that power data centers. Tesla represents exactly the category India needs: a well-funded company ($6 billion xAI funding, Tesla’s $800+ billion market cap) building cutting-edge AI chips with motivation to diversify manufacturing beyond US/China. India should use Tesla’s announcement as catalyst to aggressively court vertical integration plays from other tech giants (Google’s TPUs, Amazon’s Trainium, Microsoft’s custom silicon) rather than waiting for traditional semiconductor companies. The opportunity window is narrow—if India doesn’t attract major chip manufacturing by 2027, the country risks permanent dependence on imported semiconductors while spending $200+ billion on AI infrastructure that lacks compute hardware to fill data centers.

Why is there a chip shortage if companies like Micron are building new fabs?

The semiconductor shortage persists because AI demand is growing exponentially faster than manufacturing capacity. Micron’s announcement on March 15, 2026 of a second fab specifically targets high-bandwidth memory (HBM) used in AI GPUs—every NVIDIA H100/H200 requires specialized memory that only Micron, Samsung, and SK Hynix produce, and current production can’t meet demand from hyperscalers (Amazon, Google, Microsoft, Meta) plus AI startups globally. Building new fabs requires 2-4 years from groundbreaking to production—Micron’s new facility won’t produce chips until 2028-2029. Meanwhile, AI companies need chips NOW for training GPT-5, Gemini 3, Llama 4, Claude 4, and hundreds of other models. India faces acute shortage impact: the $200+ billion AI infrastructure commitments (Adani $100B, Microsoft $50B, others) assume GPU availability, but global allocation prioritizes existing hyperscaler customers. IndiaAI Mission’s 18,693 GPUs cost ₹2,400 crore; scaling to 1.8 million GPUs requires ₹2.4 lakh crore ($30B)—unfunded in current budgets. Shortage won’t resolve until 2027-2028 when new fabs complete, creating 18-24 month window where India’s AI ambitions face compute constraints.